This piece was published in the 31st print volume of the Asian American Policy Review.

Much of the work on wealth status to date has focused on comparing Asian Americans to other racial groups using a dichotomy that typically posits Asian Americans and Whites against Latinos and African Americans on the lower end of the wealth distribution. This framework limits and misconstrues the reality that many Asian Americans face, particularly those that are newer immigrants.

Abstract

This paper expands on existing research by providing a more in depth and nuanced analysis of wealth within the Asian American community by considering foreign-born status and ethnicity. By a number of traditional aggregate wealth indicators (e.g., income, home ownership, entrepreneurship) Asian Americans are at or near parity with non-Hispanic whites (NHWs). However, this dichotomy buries some critical disparities among AAs and may lead policymakers and scholars to exclude Asian Americans from asset building policies targeting racial minorities and disadvantaged groups. Using data from the Survey of Income and Program Participation we find a notable portion of Asian Americans at the higher and lower ends of the wealth distribution demonstrating large disparity of wealth within the Asian American community. With data from the Census American Community Survey, we find that foreign born status and ethnicity as key to explaining this disparity. Our findings suggest policies and programs that focus on and target the most vulnerable Asian Americans at the bottom of the wealth quartile, newer immigrants, and Southeast Asians.

1. Introduction

While much of the scholarly research continues to demonstrate the economic success of Asian Americans, there is also evidence of Asian American economic disparity.[i]Much of the work on wealth status to date has focused on comparing Asian Americans to other racial groups using a dichotomy that typically posits Asian Americans and Whites against Latinos and African Americans on the lower end of the wealth distribution.[ii]This framework limits and misconstrues the reality that many Asian Americans face, particularly those that are newer immigrants. Popular media such as the film “Crazy Rich Asians” also perpetuate the model minority myth, which can be detrimental to understanding the vast inequality within the community which policy can address. As an alternative policy framework, this article provides a more in depth and nuanced approach, which considers its ethnic diversity and historical context.[iii]

The Asian-White wealth gap has fluctuated over time, disappearing in 2005 because of the housing boom, but subsequently widening as the Great Recession wiped out wealth gains made by Asian Americans.[iv]In 2009, Asian Americans were behind Non-Hispanic whites in overall wealth,[v] Despite findings that show Asian Americans exceeding Non-Hispanic Whites on other economic measures such as household income. Income has not translated into wealth for Asian Americans as it has for Non-Hispanic whites. There are several explanations for why the wealth gap persists, including differences in ethnicity, immigration history and various historical experiences of Asian Americans in the United States.

Few studies have examined predictors of wealth among Asian subgroups. Existing studies either focus solely on immigrants, or they provide descriptive statistics on a few larger groups.[vi]Much of this lacuna is due to a lack of publicly available statistics, due partly to small sample size. This paper addresses these limitations by using micro-level data, which enables us to estimate predictors of wealth including nativity for Asian American ethnic groups using an indirect measure of wealth, income from interests, dividends, and rental income. This refined analysis provides a more holistic picture of Asian American wealth that encourages equitable policy and programs targeted to those who need it most.

2. Prior Research

There is a small but growing body of research examining predictors of wealth for Asians and Asian Americans.[vii] This research generally concludes that wealth levels are close to or exceeding that of non-Hispanic Whites.[viii]These findings might be expected because on average Asian Americans have higher levels of education and income.[ix] After controlling for wealth determinants, some studies still find an Asian and White wealth gap.[x] Essentially, higher levels of education and income are not translating into wealth at a commensurate level for Asian Americans compared to their non-Hispanic White counterparts. This finding is consistent with studies showing that a lower rate of return on earnings from education for Asian Americans, particularly males.[xi]

There are several explanations for group differences in wealth. One of the most influential works on African Americans and Whites is Oliver and Shapiro’s Black Wealth/White Wealth.[xii] They expanded understanding about the structural and historical factors that influence wealth status, especially the transfer of intergenerational wealth. Long standing discrimination in housing and financial markets such as redlining, zoning, and subprime lending contributed to different opportunities to build wealth.[xiii]

Historically, racial discrimination has also impacted Asian Americans. For instance, the first zoning law in the United States was directed at Chinese Americans growing their laundry businesses in California.[xiv] Discrimination in the housing market is especially important as Asian Americans, like other racial minorities, continue to hold most of their wealth in homeownership (opposed to stocks, rental income, other assets, etc.) compared to whites.[xv] It has been noted that racial discrimination based on skin color including darker-skinned Asian Americans, as well as discrimination based on accent, which affects foreign-born Asians and Asian Americans negatively.[xvi]

Like the Latinx population, Asian Americans have been impacted by immigration policies which favor certain groups over others.[xvii] The most influential policies in shaping the distribution have been (1) economic selection; (2) refugee policy; and (3) family reunification. This has manifested into ethnic differences in wealth. Some ethnic groups came and continue to enter the United States by bringing capital investment or by filling highly skilled occupations.[xviii] These Asian immigrants such as Asian Indians and Chinese, arrive ready to ride the wave of the new economy, contributing their skills, knowledge, and dollars to the United States.[xix] In comparison, political refugees from Southeast Asia have come with few economic resources, to escape war and political persecution with for the most part less education and skills.[xx] Lastly, family reunification has facilitated chain migration of individuals of the same socioeconomic standing, reinforcing class differences and reproducing the same patterns of distribution of wealth among Asian Americans.[xxi] Thus, for Asian Americans, foreign-born status remains an important variable to understanding wealth differentials including those within an Asian ethnic group.

Since the Asian population in the United States remains a highly foreign-born population at 66 percent, factors related to immigration remain relevant.[xxii] Immigration status and how long one has been in the United States plays a role in behaviors, attitudes, and understanding around US financial institutions and mechanisms for generating wealth and saving. For example, English language proficiency affects how well one understands US financial institutions and policies.

Research on Asian American wealth remains limited mostly due to low sample size in national data sets and because of the popular belief that Asian Americans are a “successful” minority not in need of examination. Because of the small but growing numbers of Asian Americans, they often are grouped with other populations such as American Indian and Alaska Natives or “Other”.[xxiii] This makes it difficult to do analysis specific to the Asian American population and even more so by Asian American ethnicity. To address this challenge, newer studies have included an analysis of specific Asian American ethnic groups however to date much of this research has been descriptive and the data not publicly available. [xxiv]

3. Data and Methods

We analyze wealth patterns among Asian Americans overall and overtime using data from the Census Bureau’s 2000, 2004 and 2008 cohorts (which includes 2011 data) Survey of Income and Program Participation (SIPP).[xxv], [xxvi] Since it is primarily a tool for government planning, it does not accurately account for wealth held by households at the top end of the distribution.[xxvii] Information about country of origin is available only in some years which is why some research published has examined only Asian immigrants.[xxviii] Despite its disadvantages, the SIPP data set is the most comprehensive available for public use with a sufficient sample of Asian Americans.[xxix]

We use 2008 SIPP data from Wave 10 Core micro data, which include information on household demographic characteristics, family size, and income status. This data set includes information up to 2011. We derive wealth information (i.e., total wealth, total net wealth, total debt, etc.) from the Wave 10 Topical file. We retrieved information about foreign-born status and the number of years in the United States from the Wave 2 Topical file. We kept cases that had information for both waves, restricting to only those respondents in the fourth reference month. After joining the two waves together, there was a total sample of 17,298, which breaks down as follows: 12,763 Non-Hispanic whites; 1,958 Blacks; 1,916 Latinos; and 661 Asians.

We complement the analysis of SIPP by analyzing the Census American Community Survey Public Use Microdata Sample (ACS PUMS) 5-year (2008-2012), which enables us to analyze wealth for Asian ethnic groups, and by nativity. The ACS PUMS collects information correlated with assets in the form of income from interests, dividends, and rental income.[xxx], [xxxi]

The PUMS in the analysis included 221,435 Asian Americans, identified as the reference person, and excluded those residing in group quarters. We examine patterns for the 13 largest Asian American ethnic groups. These include 40,275 Asian Indians; 57,485 Chinese; 37,040 Filipinos; 22,168 Koreans; 21,567 Vietnamese; 17,478 Japanese; 3,725 Pakistanis; 2,701 Cambodians; 2,436 Thais; 2,158 Laotians; 1,729 Hmong; and 1,326 Bangladeshis.[xxxii]

We also use multivariate statistical models to estimate the amount of income from assets and the likelihood of having income from assets by Asian ethnicity and nativity status.[xxxiii] To estimate the predicted income from assets, we ran a Tobit regression to account for the many observations with zero values for the dependent variables (income from assets). We ran two separate models, one for native-born (US born) and one separately for foreign-born Asians. We controlled for the following variables in the native-born model: age, sex, education (years of schooling). The foreign-born model includes the same independent variables as native-born but also controls for years in the US, citizenship status, and English language proficiency.[xxxiv]

We used logistic regression to examine factors associated with the likelihood that various Asian American ethnic groups will have assets or not have assets. Japanese are used as the reference group in the model because they have the highest mean income from assets, among all Asian subgroups. This model controls for the same variables as the Tobit model: ethnicity, education, sex, age, citizenship status, and English language proficiency. Like the Tobit regression model, we estimated this model for both native and foreign-born Asian Americans.

4. Results

4.1 Wealth Inequality Among Asian Americans

When we examine the spread of wealth within the Asian American community, we find that Asian American wealth is more spread out compared to non-Hispanic whites. What this means is that there is greater inequality among Asian Americans compared to non-Hispanic whites. Table 1 shows the dollar amount of total net worth, housing equity and non-housing equity at the 25tht, 50th and 75th percentiles for Asian Americans compared to non-Hispanic Whites. The normalized spread tells us the amount of difference in wealth between those at the extreme ends of the wealth distribution (75th and 25th) standardized by those at the 50th percentile.

Table 1: United States Wealth Distribution, Asians, and Non-Hispanic whites, 2011

| Total Net Worth | Housing Worth | Nonhousing Net Worth | |||||||

| Asian | Non-Hispanic White | Asian/ Non Hispanic White | Asian | Non-Hispanic White | Asian/ Non-Hispanic White | Asian | Non-Hispanic White | Asian/ Non-Hispanic White | |

| Percentile | |||||||||

| 75th | $430,500 | $438,790 | 0.98 | $200,000 | $170,000 | 1.18 | $203,226 | $262,726 | 0.77 |

| 50th | $153,826 | $169,789 | 0.91 | $49,000 | $69,000 | 0.71 | $44,393 | $62,500 | 0.71 |

| 25th | $14,980 | $36,833 | 0.41 | 0 | 0 | $5,947 | $7,800 | 0.76 | |

| Normalized Spread | |||||||||

| 75th and 25th ratio | 28.7 | 11.9 | NA | NA | 34.2 | 33.7 | |||

| (75th-25th)/50th | 2.7 | 2.4 | 4.1 | 2.5 | 4.4 | 4.1 | |||

The ratio of the 75th percentile value for total net worth to the 25th percentile value for total net worth is 28.7 for Asian Americans compared to 11.2 for non-Hispanic whites, which also suggests greater differences among Asian Americans. The difference in spread is significant, and the current ratio for Asian Americans represents an increase compared to 2005 data that showed a 15.0 ratio for Asian Americans compared to an 11.0 ratio for Non-Hispanic whites.[xxxv] This means that after the housing boom, inequality between Asian Americans increased.

The normalized spread shows a similar pattern where Asians have a slightly higher spread than non-Hispanic Whites in terms of total net worth; 2.7 compared to 2.4 for non-Hispanic Whites. The difference in spread was more prominent when we look at the worth of housing which was 4.1 for Asian Americans compared to 2.5 for non-Hispanic Whites. The non-housing net worth also showed Asian Americans with greater difference between those at the 75th and 25th percentile with a slightly larger spread compared to non-Hispanic whites; Asian American non housing net worth ratio was 4.4 compared to 4.1 for non-Hispanic whites.

Table 1 also allows for a comparison of actual dollar amounts between the two groups and for various types of wealth holdings. The bottom 25th percentile of Asian Americans fare much worse than their non-Hispanic White counterparts. The total net worth for the bottom 25th percentile for non-Hispanic whites was more than twice the amount for Asian Americans; $36,833 compared to $14,980 The gap was smaller for other net worth (non-housing), where the difference was smaller; $5,947 for Asians at the 25th percentile compared to $7,800 for non-Hispanic whites at the 25th percentile. Overall, non-Hispanic Whites at the 75th percentile have a higher total net worth and non-housing net worth. In comparison, Asian Americans at the 75th percentile have a higher housing worth, which again reinforces the finding that racial minorities hold most of their wealth in housing.

4.2 Wealth Differences Between Asian American Groups

Table 2 presents a parity index to compare the relative difference between Asian ethnic groups relative to the average for all Asians. To calculate the ratios, we took the mean value of the wealth indicator for each Asian ethnic group and divided that by the average for all Asians. For example, the mean interest and dividend, and/or rental income for all Asians is $3,111. The parity index shows that Filipino mean interest and dividend and/or rental income mean is 51 percent of $3,111.

Table 2: Mean Household Income and Assets in the United States by Asian Ethnicity, 2008-2012

| Mean Household Income | Mean Interest, Dividend, and Rental Income | % Homeowner | Mean Home Value | |

| All Asians | $94,521 | $3,111 | 58% | $247,196 |

| Parity Index (Relative to all Asians) | ||||

| Asian Indian | 1.29 | 1.09 | 0.94 | 0.98 |

| Cambodian | 0.66 | 0.22 | 0.84 | 0.48 |

| Chinese | 1.01 | 1.48 | 0.84 | 1.29 |

| Filipino | 1.02 | 0.51 | 1.07 | 0.91 |

| Hmong | 0.60 | 0.04 | 1.07 | 0.31 |

| Japanese | 0.97 | 1.72 | 0.77 | 1.22 |

| Korean | 0.83 | 0.96 | 1.10 | 0.90 |

| Laotian | 0.68 | 0.21 | 0.82 | 0.48 |

| Pakistani-Bangladeshi | 0.94 | 0.71 | 0.88 | 0.76 |

| Thai | 0.76 | 0.57 | 1.01 | 0.69 |

| Vietnamese | 0.80 | 0.43 | 0.88 | 0.81 |

| Other Asian | 0.88 | 0.81 | 0.92 | 0.83 |

Notes: “Mean Income” and “Mean, Interest, Dividend, and Rental Income” include negative (indicating loss) and zero-dollar amounts (indicating no income). “Mean Home Value” includes those who do not own their own home (i.e., renters). For those who do not own their home, home value was set to zero.

Consistent with Ong and Patraporn (2006) and Patraporn, Ong and Houston (2009) this study also finds great variation in wealth by ethnicity. [xxxvi] Chinese and Asian Indians exceed or come close to parity on almost all wealth measures. In comparison, Hmong and Laotians report only half of the average for all Asians on all indicators except homeownership. Other recent studies examining Asian American wealth by ethnicity report similar findings; Japanese Americans are six times more likely to hold wealth than Vietnamese Americans. “Chinese Americans hold key financial assets, at a rate that is roughly five times that of Vietnamese Americans.” [xxxvii]

4.3 Predicted Income from Assets Among Foreign Born

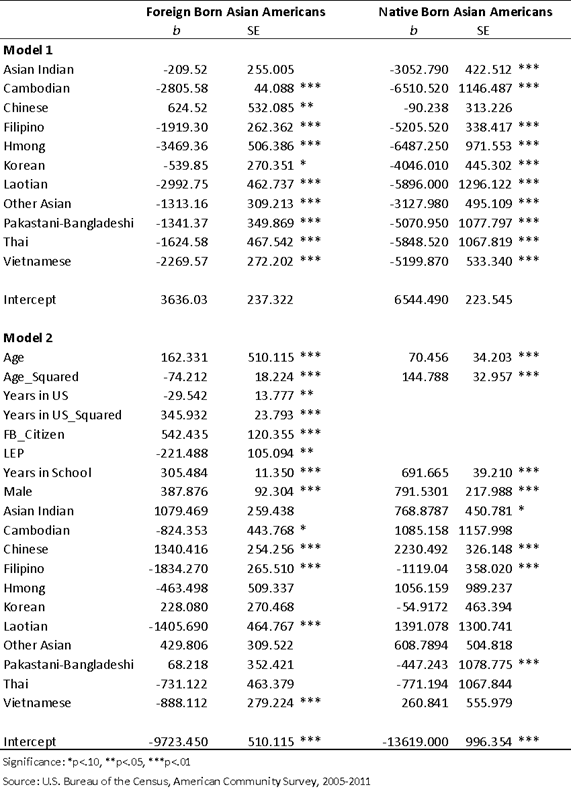

Overall, ethnic differences in income from assets among foreign born exist, but the significance of ethnicity for all groups remains mixed once we control for other wealth factors. (see Table 3). Model 1 shows that being any other Asian ethnic group compared to being Japanese results in less wealth. These findings are all statistically significant. In comparison, Model 2 (once we add control variables) shows that ethnic differences remain significant only for Cambodians, Chinese, Filipinos, Laotians and Vietnamese compared to Japanese; Cambodians (b=-824.35, p<.10), Filipinos (b=-1834.27, p<.01), Laotian (b=-1405.69, p<01), and Vietnamese (b=-888.11, p<.01).

Table 3: Tobit Model Results, 2008-2012

Being Asian Indian, Pakistani-Bangladeshi, Chinese, Korean or Other Asian results in a higher amount of assets but none of these findings are statistically significant except for Chinese (b=1340.41, p<.01). We also find ethnic differences between groups (not including Japanese as the reference group). For example, the difference in income from assets for Cambodian and Chinese is just over two thousand dollars.

As expected, findings in Model 2 demonstrate that having more education, years in the US and being male opposed to female results in more income from assets. These findings are statistically significant. Similarly, as expected being a citizen increases the amount of income from assets (542.44, p<.01) and having limited English proficiency decreases the amount of assets (-221.49, p<.05).

4.4 Ethnic Differences Predicted Income from Assets Among Native Born

Overall, the results show that ethnic differences in income from assets exist, but the significance of ethnicity remains only for certain groups after controlling for other factors related to wealth. Model 1 (Table 3) shows that coefficients for all ethnic groups are statistically significant except for Chinese. After controlling for key variables related to wealth (see Model 2), the coefficients remain significant only for Asian Indian, Pakistani-Bangladeshi, Chinese and Filipino. Native born Asian Indians and Chinese Americans have more income from assets compared to Japanese Americans net of all other factors. In contrast, Filipinos and Pakistani-Bangladeshi display less income from assets compared to native born Japanese Americans (b=-1119.04, p<.01 and b=-447.24, p<.10, respectively). We also see ethnic differences between other groups that are not Japanese such as, Chinese and Filipino representing a difference of about $2,400. As expected, we find that being male and having more education increases the amount of income from assets. These findings are both statistically significant.

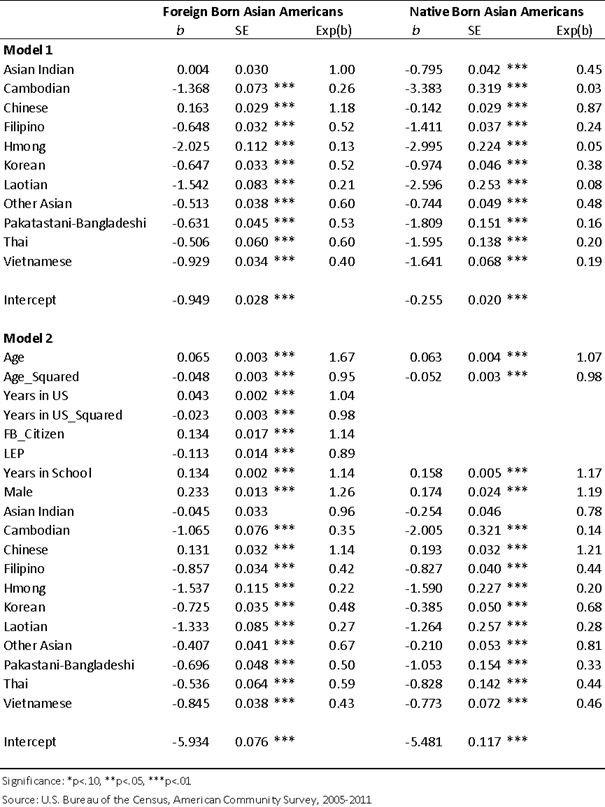

4.5 Ethnic Differences in the Odds of Having Income from Assets Among Foreign Born

Differences between Asian groups also appeared in the logistic regression results. Almost all other Asian ethnic groups regardless of nativity experience a lower likelihood of having positive net assets from secondary income compared to Japanese Americans. Table 4 shows the results from the logit model for both foreign born and native-born Asian Americans with and without controlling for a set of independent variables. Model 1 shows that for the most part Japanese have a higher likelihood of wealth relative to all other ethnic groups regardless of whether they are foreign born or native born; the two exceptions are in the case of foreign-born Chinese and Asian Indians which have the same likelihood or higher of having wealth (odds ratio=1.18 and odds ratio=1.00). These findings are highly statistically significant.

Table 4: Logit Model Results, 2008-2012

Even after controlling for key wealth factors such as age, years in school, sex, and Asian ethnicity (see Model 2) ethnicity remains significant. All Asian ethnic groups (except Chinese) showed lower odds of having positive net assets compared to foreign-born Japanese. Apart from Asian Indians, all ethnic differences between various Asian ethnic subgroups and Japanese are statistically significant (see Table 4).

All foreign-born Southeast Asian refugee groups have significantly lower odds of having positive net assets compared to Japanese Americans. For example, the odds of having positive assets for a foreign-born Hmong compared to a foreign-born Japanese net of all other factors is reduced by 88 percent. Similarly, the odds of having positive net assets for a foreign-born Laotian or Cambodian is reduced by 84 percent and 79 percent respectively compared to being Japanese holding all other factors constant. These findings are all highly statistically significant.

For foreign born Asian Americans Model 2 includes years in the US, citizenship status, and English language proficiency. As foreign-born Asians age and the longer they remain in the US their odds of having wealth goes down slightly. This is consistent with the life cycle which purports that as individuals get older and closer to retirement age wealth will begin to decrease as one is no longer working. The same is true for years in the US (b=.043) and for years in the US squared (b=-.0023). As expected, being male compared to being female increases the chances of positive net assets (odds ratio 1.26; p<.01) for foreign born Asians controlling for all other factors. Being a citizen compared to not a citizen improves the odds of having wealth (odds ratio=1.14, p<.01) net of all other factors. In addition, foreign born individuals who have limited English proficiency compared to those that have some or higher also show slightly lower odds of holding wealth (odds ratio=.89, p<.01).

4.6 Ethnic Differences in the Odds of Having Income from Assets for Native Born

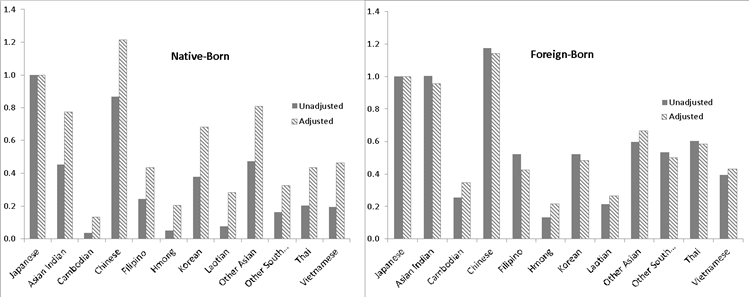

When we examine results for those native-born Asian Americans, we find a slightly different pattern with some ethnic groups experiencing substantial gains in income from assets once we control age, years in school and sex. Despite such gains, the pattern of which groups have lower or higher odds of wealth compared to Japanese Americans remains the same. Overall, ethnic differences in odds of having income from assets exist for each group compared to Japanese Americans; all coefficients for ethnicity are statistically significant except for Asian Indians. The only ethnic group to have higher odds of wealth compared to native born Japanese Americans are Chinese Americans (odds ratio=1.33, p<.01); Asian Indians, Pakistani-Bangladeshi, Filipinos, and Koreans all have lower odds of wealth compared to Japanese Americans (see Figure 1 adjusted columns).

Figure 1. Likelihood of Having Positive Income from Assets (Reference Group=Japanese), 2008-2012

Source: Tabulations by authors using Census ACS PUMS 2008-2012. Notes: Positive income from assets includes interest, dividends and/or rental income. For purposes of interpreting the odds ratios, Japanese Americans are the reference group due to their having the highest mean for interest, dividends and/or rental income compared to all other Asian groups. “Other South Asian” includes both Pakistani and Bangladeshi.

Again, Southeast Asian populations showed lower odds of having wealth compared to their Japanese counterparts with the most prominent finding being that being Cambodian compared to Japanese lowers the odds of having positive assets by 91 percent net of all other factors Similarly, being Hmong lowers the odds by 87 percent and being Laotian lowers the odds of by 80 percent.

5. Future Research

While this research shows ethnic differences in wealth, it is not clear why certain groups vary on wealth measures. Policymakers and researchers would benefit from studies which explore cultural differences in approaches to and attitudes about wealth building including consumption and savings patterns. It would also be important to understand groups that have been successful and the mechanisms that work in their favor as well as the specific challenges that other groups face. Overtime, Southeast Asian refugees have shown progress in wealth, yet for some groups the gap with other Asian groups remains alarming. Similarly, for some groups such as Filipinos we would expect higher levels of wealth or wealth at more comparable levels to Japanese, yet we find their wealth status to be lower.

A second area of future research would be to examine financial institutions such as banks and their role in the provision of wealth building services and programs. Presumably those groups that have better access to financial institutions that understand their culture would also show greater wealth accumulation. As a highly foreign-born population, the existing research on Asian Americans and financial institutions providing services in the language is notable.[xxxviii] To our knowledge, what has not been done is a comparative study of how access to such institutions might differ by Asian ethnicity. Additionally, while there has been some research focusing on banking in the Chinese and Korean communities, less is known about what kind of formal and informal institutions exist for other communities. The use of informal, alternative financial institutions or non-traditional financial institutions by ethnicity is less clear, although we know as a group that Asian Americans may use remittances as a form of alternative financial service.[xxxix], [xl]

A third area worthy of further study is why certain ethnic groups are disproportionately at risk for foreclosures. For example, in 2011 Southeast Asian Americans in the Central Valley accounted for 5 percent of all Notices of Default, a rate disproportionately higher than their proportion of the total population.[xli]Similarly, in 2009 Chaya CDC in New York found that 53 percent of Notices of Default were sent to South Asian Americans in Queens, New York, where they comprised only 13 percent of the neighborhood’s population.[xlii] In Los Angeles, Ong, Pech, and Pfeiffer (2014) estimated that Filipinos (11 percent), Koreans (10 percent), and Cambodian Americans (9 percent) were the most impacted by foreclosures among Asian American ethnic groups, with foreclosure rates more than four times that of Asian Americans overall (4 percent).[xliii] These examples demonstrate a need to better understand ethnic differences as it relates to maintaining assets as well.

6. Discussion and conclusion

Asian Americans continue to have a wealth gap in relation to Non-Hispanic Whites. Moreover, their wealth appears to be more tenuous as gains made from before the housing boom in 2005 diminish by 2012 with the most substantial change occurring with housing debt. This change in wealth is likely linked to the geographic concentration of Asian Americans in areas where the housing boom saw the greatest increases in home value but also the greatest decreases.

Moreover, there continues to be a large disparity between the top wealth holders and those at the bottom. We find that immigration and factors related to immigration to be significant in wealth building. Years in the US and English language proficiency continue to have a significant impact and thus, policies aimed at wealth accumulation among Asian Americans should continue to focus on more recent immigrants and those with less English language proficiency.

In addition, our findings also suggest that we should focus on particular ethnic groups. Differences by ethnicity appear consistently for foreign born Asian Americans across our analysis. Among native born Asian Americans, we also find statistically significant differences by ethnicity when we examine the odds of having income from assets holding key factors related to wealth constant. The groups that typically hold higher amounts of and greater likelihood of wealth are Asian Indian, Chinese, and Japanese. In comparison, Southeast Asian groups consistently show less assets and lower probabilities for having assets. Filipinos, Koreans, Pakistani-Bangladeshi and other Asians fall in between and vary in terms of their position in both amount of wealth and odds. Thus, policymakers should focus their efforts on such groups with perhaps a tiered approach based on differences.

Despite the limitations of this study, the results enhance the understanding of Asian American wealth and the factors that impact such wealth. Furthermore, findings confirm the level of disparity within the Asian American community that policy makers should note. In addition, results point to the continuing significance of ethnicity and nativity in asset building. Particular attention should be paid to those in the bottom quartile of the wealth distribution as well as those that are foreign born. Finally, our results highlight which groups and subgroups policy makers and community leaders need to focus efforts and where more research is needed to close the wealth gap.

References

[i]Christian E. Weller and Jeffery Thompson, “Wealth Inequality Among Asian Americans Greater Than Among Whites,” Center for American Progress, 20 Dec. 2016, https://www.americanprogress.org/issues/race/reports/2016/12/20/295359/wealth-inequality-among-asian-americans-greater-than-among-whites/; Rakesh Kochhar and Anthony Cilluffo, “Income Inequality in the U.S. Is Rising Most Rapidly Among Asians,” Pew Research Center, 12 July 2018, https://www.pewresearch.org/social-trends/2018/07/12/income-inequality-in-the-u-s-is-rising-most-rapidly-among-asians/.

[ii] Rebecca Tippett, PhD., Beyond Broke: Why Closing the Racial Wealth Gap is a Priority for National Economic Security (Washington, DC: Center for Global Policy Solutions, 2014) [PDF file], https://globalpolicysolutions.org/wp-content/uploads/2014/04/BeyondBroke_Exec_Summary.pdf.

[iii] Melany De La Cruz-Viesca, Darrick Hamilton, and William A. Darity, Jr., “Reframing the Asian American Wealth Narrative: An Examination of the Racial Wealth Gap in the National Asset Scorecard for Communities of Color Survey,” AAPI Nexus: Policy, Practice and Community 13, no. 1–2 (2015): 1–13. https://doi.org/10.17953/1545-0317.13.1.1

[iv] R. Varisa Patraporn, Paul M. Ong, and Douglas Houston, “Closing the Asian-White Wealth Gap?” Asian American Policy Review, vol. 18 (2009): 35–48. https://go.gale.com/ps/anonymous?id=GALE%7CA210520238&sid=googleScholar&v=2.1&it=r&linkaccess=abs&issn=10621830&p=AONE&sw=w.; Tippett et al., “Beyond Broke.”

[v] Tippett et al., “Beyond Broke.”

[vi] Lingxin Hao, Color Lines, Country Lines: Race, Immigration, and Wealth Stratification in America (New York: Russell Sage Foundation, 2007), https://www.jstor.org/stable/10.7758/9781610442688#:~:text=Workspace-,Color%20Lines%2C%20Country%20Lines%3A%20Race%2C%20Immigration%2C,and%20Wealth%20Stratification%20in%20America&text=Book%20Description%3A&text=In%20Color%20Lines%2C%20Country%20Lines,in%20the%20ways%20commonly%20believed..; Lisa A. Keister, Jody Agius Vallejo, and Brian Aronson, “Chinese Immigrant Wealth: Heterogeneity in Adaptation,” PLoS ONE 11, no. 12 (2016): 1–23. https://doi.org/10.1371/journal.pone.0168043; Pew Research Center, The Rise of Asian Americans; De La Cruz-Viesca et al., “Reframing the Asian American Wealth Narrative.”

[vii] Lingxin, Color Lines, Country Lines; Keister et al., “Chinese Immigrant Wealth”; Patraporn et al., “Closing the Asian-White Wealth Gap?”; Paul Ongl and Varisa Patraporn, “Asian Americans & Wealth,” in Wealth Accumulation & Communities of Color in the United States: Current Issues (Ann Arbor, MI: University of Michigan Press, 2006), 173–88; Paul M. Ong, Chhandara Pech, and Alycia Cheng, “Wealth Heterogeneity Among Asian American Elderly,” Asian American Policy Review 27, (2017 2016): 1–22.

[viii] Ong and Patraporn, “Asian Americans & Wealth.”; Patraporn et al., “Closing the Asian-White Wealth Gap?”; Rakesh Kochhar and Richard Fry, “Wealth Inequality Has Widened Along Racial, Ethnic Lines since End of Great Recession,” Pew Research Center, 2014, https://www.pewresearch.org/fact-tank/2014/12/12/racial-wealth-gaps-great-recession/; Tippett et al., “Beyond Broke.”

[ix] José-Víctor Ríos-Rull, Javier Díaz-Giménez, and Andy Glover, “Facts on the Distributions of Earnings, Income, and Wealth in the United States: 2007 Update,” Federal Reserve Bank of Minneapolis Quarterly Review 34, no. 1 (2007): 2–31; Maury Gittleman and Edward N. Wolff, “Racial Differences in Patterns of Wealth Accumulation,” The Journal of Human Resources 39, no. 1 (2004): 193–227. https://doi.org/10.2307/3559010; Lisa A. Keister, “Race and Wealth Inequality: The Impact of Racial Differences in Asset Ownership on the Distribution of Household Wealth,” Social Science Research 29, no. 4 (2000): 477–502. https://doi.org/10.1006/ssre.2000.0677; Martha N. Ozawa, Jeounghee Kim, and Myungkook Joo, “Income Class and the Accumulation of Net Worth in the United States,” Social Work Research 30, no. 4 (2006): 211–22; Edward N. Wolff, “Inheritances and Wealth Inequality, 1989-1998.” The American Economic Review 92, no. 2 (2002): 260–64.

[x] Lori Ann Campbell, and Robert L. Kaufman, “Racial Differences in Household Wealth: Beyond Black and White,” Research in Social Stratification and Mobility 24, no. 2 (April 1, 2006): 131–52. https://doi.org/10.1016/j.rssm.2005.06.001; Patraporn et al., “Closing the Asian-White Wealth Gap?”

[xi] Chang Hwan Kim and Arthur Sakamoto, “Have Asian American Men Achieved Labor Market Parity with White Men?” American Sociological Review 75, no. 6 (2010): 934–57. https://doi.org/10.1177/0003122410388501; Deborah Woo, Glass Ceilings and Asian Americans: The New Face of Workplace Barriers (Lantham, MD: Rowman and Littlefield, 2000).

[xii] Melvin L Oliver, Black Wealth/White Wealth: A New Perspective on Racial Inequality (New York: NY: Routledge, 1995).

[xiii] James A. Berkovec et al., “Race, Redlining, and Residential Mortgage Loan Performance,” The Journal of Real Estate Finance and Economics 9, no. 3 (November 1,1994): 263–94. https://doi.org/10.1007/BF01099279; Derek S Hyra et al., “Metropolitan Segregation and the Subprime Lending Crisis,” Housing Policy Debate: Assessing the Foreclosure Crisis From the Ground Up 23, no. 1 (2013): 177–98. https://doi.org/10.1080/10511482.2012.697912; John Yinger, “Why Default Rates Cannot Shed Light on Mortgage Discrimination,” Cityscape 2, no. 1 (1996): 25–31; Dan Immergluck, and Geoff Smith, “Measuring the Effect of Subprime Lending on Neighborhood Foreclosures: Evidence from Chicago,” Urban Affairs Review 40, no. 3 (January 1, 2005): 362–89. https://doi.org/10.1177/1078087404271444; Gary Arthur Dymski, “The Theory of Bank Redlining and Discrimination: An Exploration,” The Review of Black Political Economy 23, no. 3 (March 1, 1995): 37–74. https://doi.org/10.1007/BF02689991; Geoffrey M. B. Tootell, “Redlining in Boston: Do Mortgage Lenders Discriminate Against Neighborhoods?” The Quarterly Journal of Economics 111, no. 4 (1996): 1049–79. https://doi.org/10.2307/2946707; Gary Dymski, Jesus Hernandez, and Lisa Mohanty, “Race, Gender, Power, and the Us Subprime Mortgage and Foreclosure Crisis: Ameso Analysis,” Feminist Economics 19, no. 3 (July 2013): 124–51. https://doi.org/10.1080/13545701.2013.791401.

[xiv] Paul Ong, “An Ethnic Trade: The Chinese Laundries in Early California,” Journal of Ethnic Studies 8, no. 4 (1981): 95–113.

[xv] Z. Di, “The Role of Housing as a Component of Wealth,” Northwestern Joint Center for Poverty, Working Paper Series, no. 16, (2001); Richard Fry, Rakesh Kochhar, and Paul Taylor, “Wealth Gaps Rise to Record Highs Between Whites, Blacks, Hispanics,” Pew Research Center’s Social & Demographic Trends Project, 26 July 2011. https://www.pewsocialtrends.org/2011/07/26/wealth-gaps-rise-to-record-highs-between-whites-blacks-hispanics/.

[xvi] Matthew A. Painter, Malcolm D. Holmes, and Jenna Bateman, “Skin Tone, Race/Ethnicity, and Wealth Inequality among New Immigrants,” Social Forces 94, no. 3 (March 1, 2016): 1153–85. https://doi.org/10.1093/sf/sov094.

[xvii] Lingxin Hao, “Wealth of Immigrant and Native-Born Americans,” The International Migration Review 38, no. 2 (2004): 518–46.

[xviii] John M. Liu, Paul M. Ong, and Carolyn Rosenstein, “Dual Chain Migration: Post-1965 Filipino Immigration to the United States,” International Migration Review 25, no. 3 (September 1, 1991): 487–513. https://doi.org/10.1177/019791839102500302.

[xix] Yen-Fen Tseng, “Beyond ‘Little Taipei’: The Development of Taiwanese Immigrant Businesses in Los Angeles,” International Migration Review 29, no. 1 (March 1, 1995): 33–58. https://doi.org/10.1177/019791839502900103; Yen-Fen Tseng, “The Mobility of Entrepreneurs and Capital: Taiwanese Capital-Linked Migration,” International Migration 38, no. 2 (2000): 143–68. https://doi.org/10.1111/1468-2435.00105; Rebecca Kim, and Min Zhou, “A Tale of Two Metropolises: New Immigrant Chinese Communities in New York and Los Angeles,” in New York and Los Angeles: Politics, Society, and Culture–A Comparative View (Chicago, IL: University of Chicago Press, 2003), 124–50.

[xx] Ngoan Le, “The Case of the Southeast Asian Refugees: Policy for a Community ‘at-Risk,’” in The State of Asian Pacific America: A Public Policy Report: Policy Issues to the Year 2020. (Los Angeles, CA: LEAP Asian Pacific American Public Policy Institute and UCLA Asian American Studies Center, 1993); Paul Ong and Evelyn Blumenberg, “Job Access, Commute and Travel Burden among Welfare Recipients,” Urban Studies (Routledge) 35, no. 1 (January 1998): 77–93. https://doi.org/10.1080/0042098985087.

[xxi] Paul Ong and John M. Liu, “US Immigration Policies and Asian Migration,” in The New Asian Immigration in Los Angeles and Global Restructuring, (Philadelphia, PA: Temple University Press, 1994)45–73.

[xxii] “American Community Survey 1 Year Estimate, Table B05003D Sex by Age by Nativity and Citizenship Status (Asian alone),” US Bureau of the Census, 2019.

[xxiii] Yoonmee Chang, Writing the Ghetto: Class, Authorship, and the Asian American Ethnic Enclave, (New Brunswick, NJ: Rutgers University Press, 2010); Sherman Hanna and Suzanne Lindamood, “The Decrease in Stock Ownership by Minority Households,” Journal of Financial Counseling and Planning 19, no. 2 (2008): 46-58, 94-95; David W. Rothwell and Chang‐Keun Han, “Exploring the Relationship Between Assets and Family Stress Among Low‐Income Families,” Family Relations 59, no. 4 (2010): 396–407. https://doi.org/10.1111/j.1741-3729.2010.00611.x.

[xxiv] De La Cruz-Viesca et al., “Reframing the Asian American Wealth Narrative”; Kochhar and Fry, “Wealth Inequality Has Widened”; Tippett et al., “Beyond Broke.”

[xxv] The SIPP is administered by the Census Bureau, “to collect information on source and amount of income, labor force participation, program participation and eligibility data, and general demographic characteristics of individuals and households in the U.S.”

[xxvi] “SIPP Introduction & History,” The United States Census Bureau, accessed 11 October 2020, https://www.census.gov/programs-surveys/sipp/about/sipp-introduction-history.html.

[xxvii] John L. Czajka, Jonathan E. Jacobson, and Scott Cody, “Survey Estimates of Wealth: A Comparative Analysis and Review of the Survey of Income and Program Participation,” IDEAS Working Paper Series from RePEc, 2004. http://csulb.idm.oclc.org/login?url=https://search.proquest.com/docview/1698793612?accountid=10351; Deborah A. Cobb-Clark and Vincent A. Hildebrand, “The Wealth and Asset Holdings of U.S.-Born and Foreign-Born Households: Evidence from Sipp Data,” Review of Income & Wealth 52, no. 1 (March 2006): 17–42. https://doi.org/10.1111/j.1475-4991.2006.00174.x; Di, “The Role of Housing”.

[xxviii] Hao, Color Lines, Country Lines.

[xxix] This is when compared to the other two major national surveys that track wealth: the Survey of Consumer Finance (SCF) conducted by the Federal Reserve Board, and the Panel Study of Income Dynamics (PSID) conducted by the University of Michigan, Institute for Social Research.For instance, the most recent Survey of Consumer Finance (SCF) 2011 collected data on the race of the respondent but those data are not publicly available by Asian race due to the small sample size, which could potentially cause a disclosure issue. The Panel Study of Income Dynamics also readily reports data on wealth and like the SIPP has the advantage of being a longitudinal study. However, this data set does not contain a sufficient sample of Asians nor does it make data on Asians publicly available.

[xxx] Ong et al., “Wealth Heterogeneity.”

[xxxi] PUMS is an individual-level subsample of ACS data, covering approximately 1 percent of the population annually. The PUMS file covering a five-year period contains data on approximately 5 percent of the population. PUMS data, as opposed to summary data, contain the individual responses for a subsample of the ACS housing units, and the people in the selected housing units. Using micro-data allows for custom sample universes and detailed relationships among variables to be drawn, and that may not be shown in standard summary data.

[xxxii] All other Asian ethnic groups were categorized as “other Asian.” Due to the smaller sample size of Bangladeshis and a similar history and culture, we combined Bangladeshi and Pakistani together for purposes of regression analysis.

[xxxiii] Assets are defined as positive income generated from interest, dividend, and rental income.

[xxxiv] Years in the US was computed by subtracting the year of entry into the US from the year of the ACS survey. We defined limited English proficiency as those who self-reported that they spoke English “less than very well.” Those individuals who are not citizens include documented and undocumented foreign-born persons, although there is no way to distinguish the two in the PUMS dataset.

[xxxv] Patraporn et al., “Closing the Asian-White Wealth Gap?”

[xxxvi] Ong, and Patraporn. “Asian Americans & Wealth.”; Patraporn, Ong, and Houston. “Closing the Asian-White Wealth Gap?”.

[xxxvii] Tippett et al. “Beyond Broke”. Tippett et al. “Beyond Broke” pg. 5.

[xxxviii] National CAPACD, National Urban League, and National Council of La Raza, “Banking in Color: New Findings on Financial Access for Low- and Moderate-Income Communities,” 2014. https://www.nationalcapacd.org/uncategorized/banking-color-new-findings-financial-access-low-moderate-income-communities/.

[xxxix] Ibid.

[xl] About 22 percent of Asian American and Pacific Islander low- and moderate-income survey respondents used remittances or wire transfers—a rate slightly higher than Latinos (17 percent)—and the third most used alternative financial service, following credit cards from a bank and gift cards.

[xli] National Coalition for Asian Pacific American Community Development, (National CAPACD), and (SEARAC) Southeast Asia resource Action Center, “Untold Stories of the Foreclosure Crisis: Southeast Asian Americans in the Central Valley,” April 2011. https://www.firminc.org/wp-content/uploads/2011/05/SEARAC_CRISIS_REPORT_2011_Final.pdf.

[xlii] Chhaya Community Development Coalition “Fifty Percent of Homes in Pre-Foreclosure Are Owned by South Asian Immigrants in Sections of New York City,” January 12, 2009.

[xliii] Paul M Ong, Chhandara Pech, and Deirdre Pfeiffer, “The Foreclosure Crisis in Los Angeles,” UCLA Luskin School of Public Affairs Lewis Center California Policy Options 2014, 2013, 20.